When saving for college, 529 plans and Coverdell Education Savings Accounts (ESAs) are two popular options. As of June 2023,

16.25 million families1 had active 529 accounts.

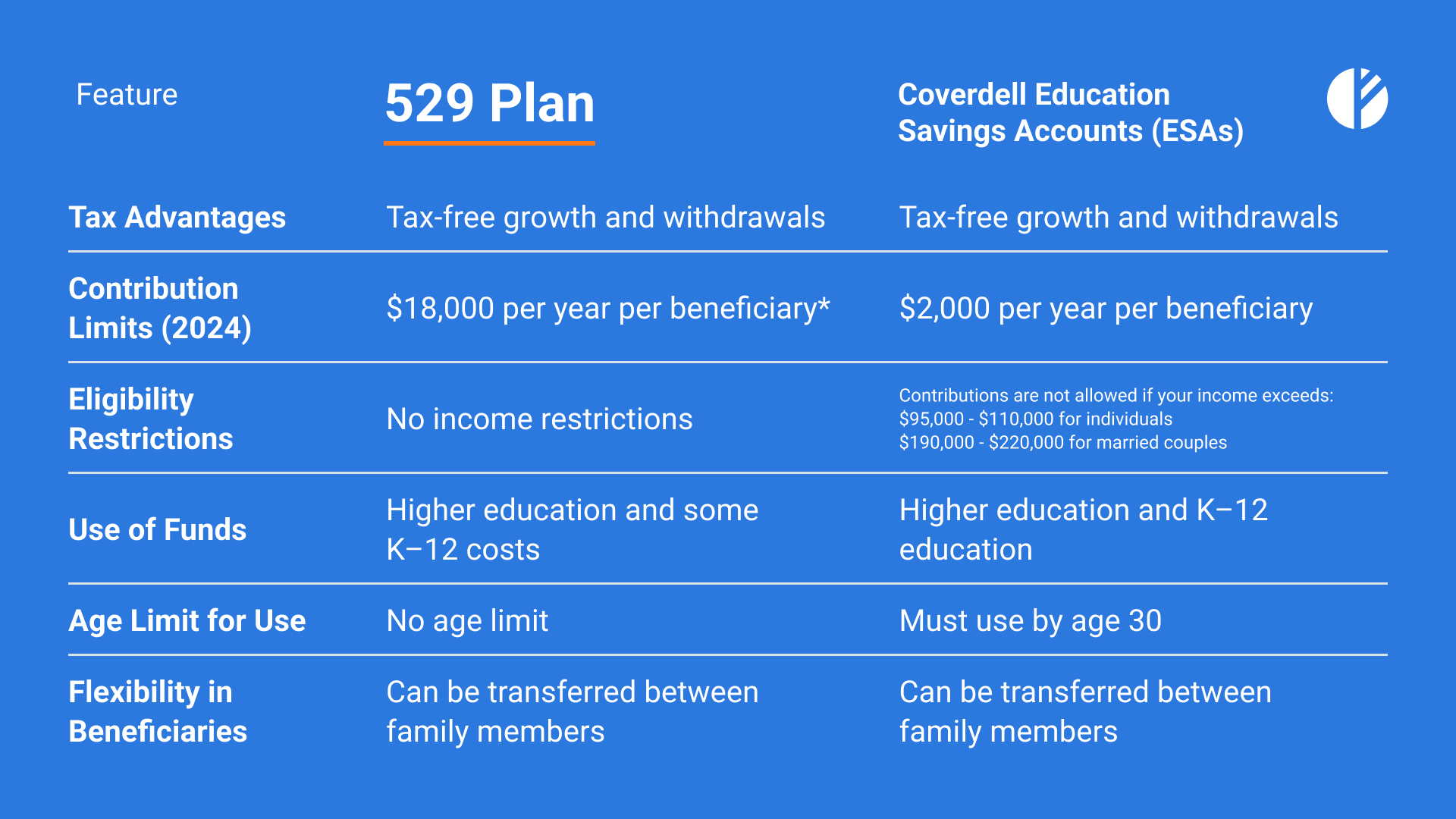

While both options offer tax advantages for education savings, the 529 plan has higher contribution limits and no income restrictions.

Gifts

* For example, in 2024, the annual gift tax exclusion was $18,000, meaning you could give this amount to individuals without affecting your lifetime gift tax exemption.

The lifetime exemption is $13.61 million for individuals and $27.22 million for couples. For 529 plans, you can contribute up to five years' worth of the annual exclusion at once without triggering gift taxes.

For instance, a grandparent could contribute $90,000 to a grandchild's 529 plan without affecting their lifetime exemption, as long as no other gifts are made for five years.

However, it’s important to note that the contribution limits of $235,000 to $575,000 are lifetime maximums – not annual caps – and vary by state. They represent the total amount a 529 plan can hold before no more contributions are accepted.

Benefits and flexibility

For families primarily focused on funding higher education, the dedicated structure of 529 plans makes them a compelling choice over alternatives. Qualified education expenses include tuition, fees, books, and supplies.

The plan can also cover room and board costs for students enrolled at least half-time. Additionally, certain technology-related expenses like computers, software, and internet access, are eligible for coverage.

If funds are withdrawn for non-qualified expenses, the earnings are subject to income tax and a 10% penalty, with exceptions for circumstances like death or disability.

While contributions to a 529 plan are not federally tax-deductible, over 30 states offer deductions or credits. The states with

the largest2 529 college savings plans include Virginia ($85 billion), New York ($38.6 billion), and Nevada ($32.6 billion).

Although many states require you to invest in your home state's plan, some allow nonresident investments without a tax break. According to the College Savings Plans Network, the average total balance in 529 plans was approximately $28,000 per beneficiary last year.

There are two basic types of 529 plans:

1. Education savings plans

- Variety of investment options

- Withdrawals are tax-free

- Controlled by the donor, usually a parent

2. Prepaid tuition plans

- Withdrawals are tax-free

- Don't cover K–12 education or room and board

- May restrict eligible institutions

- Funds may not be federally guaranteed

Prepaid Tuition Plans allow account holders to purchase credits at today’s tuition rates, locking in future education costs at eligible institutions. Given the rising costs of tuition, this generally means locking in lower prices for college later.

For example, in 2023, tuition rates were increasing at an average annual rate of around 2.5% to 4%.

With high contribution limits, no income requirements, and coverage for a variety of eligible expenses, 529 plans offer a flexible option for families seeking long-term funding for their children's education.

Imperial Fund Asset Management is a SEC-registered investment adviser.

SEC registration does not imply a certain level of skill or training.

The information provided is for informational purposes only and should not be considered investment advice or a solicitation to buy or sell any securities.

All investments involve risk, including the possible loss of principal. Please review our

full disclaimer for additional information.